Euro

2008/9 Schools Wikipedia Selection. Related subjects: Currency

| Euro EURO (Latin alphabet) ΕΥΡΩ (Greek alphabet) unofficial spelling variants exist

|

|||||

|

|||||

| ISO 4217 Code | EUR (num. 978) | ||||

|---|---|---|---|---|---|

| Official user(s) |

15

|

||||

| Unofficial user(s) | |||||

| Inflation | 3.1% | ||||

| Source | European Central Bank, January 2008 | ||||

| Method | HICP | ||||

| Pegged by |

10 currencies

|

||||

| Subunit | |||||

| 1/100 | cent actual usage varies depending on language |

||||

| Symbol | € | ||||

| Plural | See Euro linguistic issues | ||||

| cent | See article | ||||

| Coins | |||||

| Freq. used | 1, 2, 5, 10, 20, 50 cent, €1, €2 unless otherwise stated as rarely used |

||||

| Rarely used | 1 and 2 cent (applies to Finland and The Netherlands) |

||||

| Banknotes | |||||

| Freq. used | €5, €10, €20, €50 | ||||

| Rarely used | €100, €200, €500 | ||||

| Central bank | European Central Bank | ||||

| Website | www.ecb.eu | ||||

| Printer |

printers

|

||||

| Website |

websites

|

||||

The euro ( currency sign: €; banking code: EUR) is the official currency of the European Union's Eurozone, which currently consists of 15 states (Austria, Belgium, Cyprus, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, the Netherlands, Portugal, Slovenia, Spain). It is the single currency for more than 320 million Europeans. Including areas using currencies pegged to the euro, the euro directly affects close to 500 million people worldwide. With more than €610 billion in circulation as of December 2006 (equivalent to US$802 billion at the exchange rates at the time), the euro is the currency with the highest combined value of cash in circulation in the world, having surpassed the U.S. dollar.

The euro was introduced to world financial markets as an accounting currency in 1999 and launched as physical coins and banknotes on 1 January 2002. It replaced the former European Currency Unit (ECU) at a ratio of 1:1.

The euro is managed and administered by the Frankfurt-based European Central Bank (ECB) and the Eurosystem (composed of the central banks of the euro zone countries). As an independent central bank, the ECB has sole authority to set monetary policy. The Eurosystem participates in the printing, minting and distribution of notes and coins in all member states, and the operation of the Eurozone payment systems.

While all European Union (EU) member states are eligible to join if they comply with certain monetary requirements, not all EU members have chosen to adopt the currency. All nations that have joined the EU since the 1993 implementation of the Maastricht Treaty have pledged to adopt the euro in due course. Maastricht obliged current members to join the euro; however, the United Kingdom and Denmark negotiated exemptions from that requirement for themselves. Sweden turned down the euro in a 2003 referendum, and has circumvented the requirement to join the euro area by not meeting the membership criteria. In addition, several small European states (Vatican City, Monaco, and San Marino), although not EU members, have adopted the euro due to currency unions with member states. Andorra, Montenegro, and Kosovo have adopted the euro unilaterally, while not being EU members either. Switzerland and Liechtenstein continue using the Swiss franc. (cf. #Eurozone.)

Characteristics

Payments clearing, electronic funds transfer

All intra- Eurozone transfers shall cost the same as a domestic one. This is true for retail payments, although several ECB payment methods can be used. Credit/debit card charging and ATM withdrawals within the Eurozone are also charged as if they were domestic. The ECB has not standardised paper-based payment orders, such as cheques; these are still domestic-based.

The ECB has set up a clearing system, TARGET, for large euro transactions.

The currency sign €

A special euro currency sign (€) was designed after a public survey had narrowed the original ten proposals down to two. The European Commission then chose the final design. The eventual winner was a design created by the Belgian Alain Billiet. The official story of the design history of the euro sign is disputed by Arthur Eisenmenger, a former chief graphic designer for the EEC, who claims to have created it as a generic symbol of Europe.

The glyph is according to the European Commission "a combination of the Greek epsilon, as a sign of the weight of European civilization; an E for Europe; and the parallel lines crossing through standing for the stability of the euro".

The European Commission also specified a euro logo with exact proportions and foreground/background colour tones. While the Commission intended the logo to be a prescribed glyph shape, font designers made it clear that they intended to design their own variants instead.

Placement of the currency sign varies from nation to nation. There are no official standards on where to place the euro sign.

Another advantage to the final chosen symbol is that it is easily created on a typewriter lacking the euro sign, by typing a capital 'C', backspacing and overstriking it with the equal ('=') sign.

Economic and Monetary Union

History (1990–2008)

The euro was established by the provisions in the 1992 Maastricht Treaty on European Union that was used to establish an economic and monetary union. In order to participate in the new currency, member states had to meet strict criteria such as a budget deficit of less than three per cent of their GDP, a debt ratio of less than sixty per cent of GDP, low inflation, and interest rates close to the EU average. In the Maastricht Treaty, the United Kingdom and Denmark were granted exemptions from moving to the stage of monetary union which would result in the introduction of the euro.

Economists that helped create or contributed to the euro include Robert Mundell, Wim Duisenberg, Robert Tollison, Neil Dowling, Fred Arditti and Tommaso Padoa-Schioppa. (For macro-economic theory, see below.)

| Currency | Abbr. | Rate | Fixed on | EMU III |

|---|---|---|---|---|

| ATS | 13.7603 | 1998- 12-31 | 1999 | |

| BEF | 40.3399 | 1998- 12-31 | 1999 | |

| NLG | 2.20371 | 1998- 12-31 | 1999 | |

| FIM | 5.94573 | 1998- 12-31 | 1999 | |

| FRF | 6.55957 | 1998- 12-31 | 1999 | |

| DEM | 1.95583 | 1998- 12-31 | 1999 | |

| IEP | 0.787564 | 1998- 12-31 | 1999 | |

| ITL | 1936.27 | 1998- 12-31 | 1999 | |

| LUF | 40.3399 | 1998- 12-31 | 1999 | |

| PTE | 200.482 | 1998- 12-31 | 1999 | |

| ESP | 166.386 | 1998- 12-31 | 1999 | |

| GRD | 340.750 | 2000- 06-19 | 2001 | |

| SIT | 239.640 | 2006- 07-11 | 2007 | |

| CYP | 0.585274 | 2007- 07-10 | 2008 | |

| MTL | 0.429300 | 2007- 07-10 | 2008 |

Due to differences in national conventions for rounding and significant digits, all conversion between the national currencies had to be carried out using the process of triangulation via the euro. The definitive values in euro of these subdivisions (which represent the exchange rates at which the currency entered the euro) are shown at right.

The rates were determined by the Council of the European Union, based on a recommendation from the European Commission based on the market rates on 31 December 1998, so that one ECU ( European Currency Unit) would equal one euro. (The European Currency Unit was an accounting unit used by the EU, based on the currencies of the member states; it was not a currency in its own right.) Council Regulation 2866/98 (EC), of 31 December 1998, set these rates. They could not be set earlier, because the ECU depended on the closing exchange rate of the non-euro currencies (principally the pound sterling) that day.

The procedure used to fix the irrevocable conversion rate between the drachma and the euro was different, since the euro by then was already two years old. While the conversion rates for the initial eleven currencies were determined only hours before the euro was introduced, the conversion rate for the Greek drachma was fixed several months beforehand, in Council Regulation 1478/2000 (EC), of 19 June 2000.

The currency was introduced in non-physical form (travellers' cheques, electronic transfers, banking, etc.) at midnight on 1 January 1999, when the national currencies of participating countries (the Eurozone) ceased to exist independently in that their exchange rates were locked at fixed rates against each other, effectively making them mere non-decimal subdivisions of the euro. The euro thus became the successor to the European Currency Unit (ECU). The notes and coins for the old currencies, however, continued to be used as legal tender until new notes and coins were introduced on 1 January 2002.

The changeover period during which the former currencies' notes and coins were exchanged for those of the euro lasted about two months, until 28 February 2002. The official date on which the national currencies ceased to be legal tender varied from member state to member state. The earliest date was in Germany; the Mark officially ceased to be legal tender on 31 December 2001, though the exchange period lasted two months. The final date was 28 February 2002, by which all national currencies ceased to be legal tender in their respective member states. However, even after the official date, they continued to be accepted by national central banks for periods ranging from several years to forever in Austria, Germany, Ireland, and Spain. The earliest coins to become non-convertible were the Portuguese escudos, which ceased to have monetary value after 31 December 2002, although banknotes remain exchangeable until 2022.

On 1 January 2007, Slovenia joined the Eurozone.

On 1 January 2008, Malta and Cyprus joined the Eurozone.

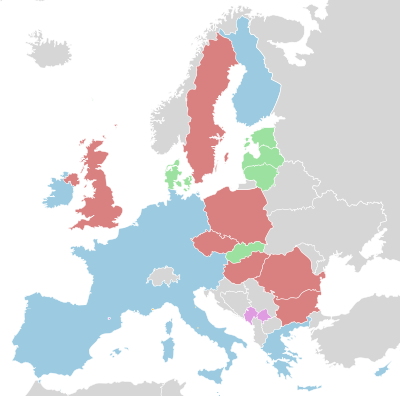

Eurozone

- The euro is the sole currency in Austria, Belgium, Cyprus, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, the Netherlands, Portugal, Slovenia and Spain. These 15 countries together are frequently referred to as the Eurozone or the euro area, or more informally "euroland" or the "eurogroup". Outside of the area covered by the map, the euro is the legal currency of the French overseas possessions of French Guiana, Réunion, Saint-Pierre et Miquelon, Guadeloupe, Martinique, Saint-Barthélemy, Saint Martin, Mayotte, and the uninhabited Clipperton Island and the French Southern and Antarctic Lands; the Portuguese autonomous regions of the Azores and Madeira; and the Spanish Canary Islands.

- By virtue of some bilateral agreements, the European microstates of Monaco, San Marino, and Vatican City mint their own euro coins on behalf of the European Central Bank. They are, however, severely limited in the total value of coins they may issue.

- Andorra, Montenegro, Kosovo, and Akrotiri and Dhekelia adopted the foreign euro as their legal currency for movement of capital and payments without participation in the ESCB or the right to mint coins. Andorra is in the process of entering a monetary agreement similar to that of the microstates above.

- Several possessions and former colonies of EU states have currencies pegged to the euro. These are French Polynesia, New Caledonia, Wallis and Futuna (the CFP franc); Cape Verde; the Comoros; and fourteen nations of Central and West Africa (the CFA franc). See Currencies related to the euro.

- Although not legal tender in Denmark and the United Kingdom, the euro is accepted in some stores throughout both countries, particularly international stores in large cities, and shops in Northern Ireland near the border with the Republic of Ireland, where the euro is the official currency. Similarly, the euro is widely accepted in Switzerland, even by official boards, such as the Swiss Railways.

Future prospects (2008–)

Pre-2004 EU members

From Greece's participation in 2001 until the EU enlargement in 2004, Denmark, Sweden and the United Kingdom were the only EU member states outside the monetary union. The situation for the three older member states also looks different from that of the newer EU members; the three countries have no clear roadmap for adopting the euro:

- Denmark negotiated a number of opt-out clauses from the Maastricht treaty after it had been rejected in a first referendum. On 28 September 2000, another referendum was held in Denmark regarding the euro resulting in a 53.2% vote against joining. However, Danish politicians have suggested that debate on abolishing the four opt-out clauses may possibly be re-opened. In addition, Denmark has pegged its krone to the euro (€1 = DKr 7.46038 ± 2.25%) as the krone remains in the ERM. Although not part of the European Union, both Greenland and the Faroe Islands use the Danish krone (the Faroes in the form of the Faroese króna), and so also fall within the ERM. Denmark will hold a new referendum by 2011.

- Sweden: Sweden is obliged to join the euro by the 1994 Act of Accession, when they meet the economic conditions. However, the krona has never been part of ERM II, rendering Sweden ineligible. In 2003, a public referendum rejected euro membership, and Sweden has no plans to adopt the euro. The EU has made it clear that it will tolerate this with respect to Sweden, thereby giving Sweden a de facto opt-out, but not those member states that joined in 2004 or 2007.

- The United Kingdom has an opt-out from eurozone membership under the Maastricht treaty and is not obliged to join the euro. While the government is in favour of membership provided the economic conditions are right (requiring that " five economic tests" be met), the general population remain opposed and the question has never been put to referendum. The United Kingdom was forced to withdraw the pound sterling from the ERM (the precursor to ERM II) on Black Wednesday ( 16 September 1992) following pressure from currency speculators, and the pound is not part of ERM II.

Post-2004 EU members

As of 2008, nine new EU member states have a currency other than the euro; however, all of these countries are required by their Accession Treaties to join the euro. Some of the following countries have already joined the European Exchange Rate Mechanism, ERM II. They and the others have set themselves the goal of joining the euro ( EMU III) as follows:

| Currency | Abbr. | Rate | Conv goal |

|---|---|---|---|

| SKK | 30.1260 | 2009- 01-01 | |

| LTL | 3.45280 | 2010- 01-01 | |

| EEK | 15.6466 | 2011- 01-01 | |

| BGN | 1.95583 | 2012- 01-01 | |

| PLN | — | 2012- 01-01 | |

| LVL | 0.702804 | 2012- 01-01 | |

| CZK | — | 2012- 01-01 | |

| HUF | — | 2012- 01-01 | |

| RON | — | 2014- 01-01 | |

| SEK | — | — |

- 1 January 2009 for Slovakia

- 1 January 2010 for Lithuania and Bulgaria

- 1 January 2011 for Estonia,

- 1 January 2012 or later for Hungary, Latvia, Czech Republic, Poland and Romania.

Too high an inflation rate postponed the entry of Lithuania and Estonia as planned on 1 January 2007. Some of these currencies do not float against the euro, and a subset of those were unilaterally pegged to the euro before joining ERM II. See European Exchange Rate Mechanism, currencies related to the euro, and individual currency articles for more details.

Originally, the Czech Republic aimed for entry into the ERM II in 2008 or 2009, but the current government has officially dropped the 2010 target date, saying it will clearly not meet the economic criteria. The new goal is 2012.

Similarly Latvia had aimed to join the euro in 2008 but inflation of over 11% has resulted in a delay as the country does not meet the current criteria. The government's official target is now 1 January 2012 although the head of the Bank of Latvia has suggested that 2013 may be a more realistic date.

The Fifth Report on the Practical Preparations for the Future Enlargement of the Euro Area stated on 16 July 2007 that only Cyprus, Malta (both of which adopted the euro in January 2008), Slovakia (2009) and Romania (2014) had currently set official target dates for adopting the euro.

Estonia, Latvia, Lithuania and Slovakia have already finalised the design for their respective coins' obverse sides.

Economics of the euro

Optimal currency areas

Economists typically cite four criteria, often called the optimum currency area (OCA) criteria, to evaluate the value of switching to a single currency. There are three economic criteria (labour and capital mobility, product diversification, and openness) and one political criterion (fiscal transfers). Since establishing a single currency over a region necessitates surrendering the ability to tailor monetary policy to local conditions, these four characteristics measure the ability of the economy to smooth local economic movements in the absence of monetary policy.

- Robert A. Mundell formulated the idea that perfect capital and labour mobility would mitigate the adverse consequences of asymmetric shocks in a currency area. While capital is quite mobile in the Eurozone, labour mobility is relatively low, especially when compared to the U.S. and Japan.

- Peter Kenen formulated the idea that widely diversified production and export structures that are similar between the areas that form the currency area lower the effect and probability of asymmetric shocks. The Eurozone scores quite well on this criterion, and monetary integration seems to further improve the diversification of production structures.

- Ronald McKinnon formulated the idea that areas which are very open to trade and trade heavily with each other form an optimum currency area. This is because the high trade intensity will lower the significance of the distinction between domestic and foreign goods as competition will equalise the prices of most goods, independently of exchange rates. The Eurozone members trade heavily with each other (intra-European trade is greater than international trade), and all evidence so far seems to indicate that the monetary union has at least doubled trade between members.

- The term " fiscal transfers" refers to the transfer of money between areas. Regions that are economically worse off or suffer from negative economic shocks receive money, creating a counter cyclical effect that lowers the price, wage, and unemployment differentials between regions. Theoretically, Europe has no bail-out clause in the Stability and Growth Pact, meaning that fiscal transfers are not allowed, but it's impossible to know what will happen in practice.

So while Europe scores well on some of the measures characterising an OCA, it has lower labour mobility than the United States and similarly cannot rely on fiscal federalism to smooth out regional economic disturbances.

Transaction costs and risks

The most obvious benefit of adopting a single currency is removing from trade the cost of exchanging currency, theoretically allowing businesses and individuals to consummate previously unprofitable trades. On the consumer side, banks in the Eurozone must charge the same for intra-member cross-border transactions as purely domestic transactions for electronic payments (e.g. credit cards, debit cards and cash machine withdrawals).

The absence of distinct currencies also removes exchange rate risks. The risk of unanticipated exchange rate movement has always added an additional risk or uncertainty for companies or individuals looking to invest or trade outside their own currency zones. Companies that hedge against this risk will no longer need to shoulder this additional cost. The reduction in risk is particularly important for countries whose currencies have traditionally fluctuated a great deal, particularly the Mediterranean nations.

Financial markets on the continent are expected to be far more liquid and flexible than they were in the past. The reduction in cross-border transaction costs will allow larger banking firms to provide a wider array of banking services that can compete across and beyond the Eurozone.

Price parity

Another effect of the common European currency is that differences in prices—in particular in price levels—should decrease because of the ' law of one price'. Differences in prices can trigger arbitrage, i.e. speculative trade in a commodity across borders purely to exploit the price differential. Therefore, prices on commonly traded goods are likely to converge, causing inflation in some regions and deflation in others during the transition. Some evidence of this has been observed in specific markets.

Macroeconomic stability

Low levels of inflation are the hallmark of stable and modern economies. Because a high level of inflation acts as a highly regressive tax ( seigniorage) and theoretically discourages investment, it is generally viewed as undesirable. In spite of the downside, many countries have been unable or unwilling to deal with serious inflationary pressures. Some countries have successfully contained them by establishing largely independent central banks. One such bank was the Bundesbank in Germany; as the European Central Bank is modelled on the Bundesbank, it is independent of the pressures of national governments and has a mandate to keep inflationary pressures low. Member countries join the bank to credibly commit to lower inflation, hoping to enjoy the macroeconomic stability associated with low levels of expected inflation. The ECB (unlike the Federal Reserve in the United States of America) does not have a second objective to sustain growth and employment.

National and corporate bonds denominated in euro are significantly more liquid and have lower interest rates than was historically the case when denominated in legacy currencies. While increased liquidity may lower the nominal interest rate on the bond, denominating the bond in a currency with low levels of inflation arguably plays a much larger role. A credible commitment to low levels of inflation and a stable debt reduces the risk that the value of the debt will be eroded by higher levels of inflation or default in the future, allowing debt to be issued at a lower nominal interest rate.

A new reserve currency

The euro is widely perceived to be a major global reserve currency, sharing that status with the U.S. dollar (USD), albeit to a lesser degree. The U.S. dollar still continues to enjoy its status as the primary reserve of most commercial and central banks worldwide.

Since its introduction, the euro has been the second most widely-held international reserve currency after the U.S. dollar. The euro inherited this status from the German mark, and since its introduction, has increased its standing somewhat, mostly at the expense of the dollar. The possibility for the euro to become the first international reserve currency in the near future is now widely debated among economists. Former Federal Reserve Chairman Alan Greenspan gave his opinion in September 2007 by stating that the euro could indeed replace the U.S. dollar as the world's primary reserve currency. He said that it is "absolutely conceivable that the euro will replace the dollar as reserve currency, or will be traded as an equally important reserve currency." Additionally, there has been some suggestion that the recent weakness of the US dollar might encourage various parties to increase their reserves in euro at the expense of the dollar. In the second term of 2007, euro as a reserve currency has reached a record level of 25.6% (a +0.8% increase from the year before)- at the expense of US dollar which dropped to 64.8% (a drop of 1.3% from the year before). By the end of 2007, shares of euro increased to 26.4% as the dollar slumped to its lowest level since records began in 1999, 63.8%.

| '95 | '96 | '97 | '98 | '99 | '00 | '01 | '02 | '03 | '04 | '05 | '06 | '07 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| US dollar | 59.0% | 62.1% | 65.2% | 69.3% | 70.9% | 70.5% | 70.7% | 66.5% | 65.8% | 65.9% | 66.4% | 65.7% | 63.3% |

| Euro | 17.9% | 18.8% | 19.8% | 24.2% | 25.3% | 24.9% | 24.3% | 25.2% | 26.5% | ||||

| German mark | 15.8% | 14.7% | 14.5% | 13.8% | |||||||||

| Pound sterling | 2.1% | 2.7% | 2.6% | 2.7% | 2.9% | 2.8% | 2.7% | 2.9% | 2.6% | 3.3% | 3.6% | 4.2% | 4.7% |

| Japanese yen | 6.8% | 6.7% | 5.8% | 6.2% | 6.4% | 6.3% | 5.2% | 4.5% | 4.1% | 3.9% | 3.7% | 3.2% | 2.9% |

| French franc | 2.4% | 1.8% | 1.4% | 1.6% | |||||||||

| Swiss franc | 0.3% | 0.2% | 0.4% | 0.3% | 0.2% | 0.3% | 0.3% | 0.4% | 0.2% | 0.2% | 0.1% | 0.2% | 0.2% |

| Other | 13.6% | 11.7% | 10.2% | 6.1% | 1.6% | 1.4% | 1.2% | 1.4% | 1.9% | 1.8% | 1.9% | 1.5% | 1.8% |

| Sources: 1995-1999, 2006-2007 IMF: Currency Composition of Official Foreign Exchange Reserves PDF (80 KB) Sources: 1999-2005, ECB: The Accumulation of Foreign Reserves PDF (816 KB) |

|||||||||||||

A currency is attractive for international transactions when it demonstrates a proven track record of stability, a well-developed financial market to trade the currency, and proven acceptability to others. While the euro has made substantial progress toward achieving these features, there are a few challenges that undermine the ascension of the euro as a major reserve currency. Persistent excessive budget deficits of some member nations, economically weak new members, conservatism of financial markets, and inertia or path dependence are all important factors keeping the euro as a junior international currency to the U.S. dollar. However, at the same time, the USD has increasingly suffered from a double deficit and consequently has its own concerns.

As the euro becomes a new reserve currency, Eurozone governments will enjoy substantial benefits. Since money is effectively an interest-free loan to the issuing government by the holder of the currency—foreign reserves act as a subsidy to the country minting the currency (see Seigniorage). However, reserve status also holds risks, as the currency may become overvalued, hurting European exporters, and potentially exposing the European economy to influence by external factors who hold large quantities of euro.

Criticism

Some European nationalist parties oppose the euro as part of a more general opposition to the European Union. A significant group of these include the members of the Independence and Democracy bloc in the European Parliament. Additionally the Green Party of England and Wales is opposed for anti-globalisation reasons but the rest of the European Green Party bloc in the European Parliament do not share their stances.

In their view, the countries that participate in the EMU have surrendered their sovereign abilities to conduct monetary policy. The European Central Bank is required to pursue a policy that might be at odds with national interests and there is no guarantee of extra-national assistance from their more fortunate neighbours should local conditions necessitate some sort of economic stimulus package. Many critics of the EMU believe the benefits to joining the organisation are outweighed by the loss of sovereignty over local policy that accompanies membership.

The euro is underpinned by the Stability and Growth Pact, which is designed to ensure even fiscal policy across the Eurozone. The SGP has been criticised for removing the ability of national governments to stimulate their own economies to a certain extent, in the only way left to them now that monetary policy is determined supranationally. The failure of some member states to observe the SGP, and its inherent problems have led to minor reforms, and further reforms are likely.

Exchange rate

Flexible exchange rates

| Year | Lowest ↓ | Highest ↑ | ||||

|---|---|---|---|---|---|---|

| Date | Rate | Date | Rate | |||

| 1999 | 03 Dec | $1.0015 | 05 Jan | $1.1790 | ||

| 2000 | 26 Oct | $0.8252 | 06 Jan | $1.0388 | ||

| 2001 | 06 Jul | $0.8384 | 05 Jan | $0.9545 | ||

| 2002 | 28 Jan | $0.8578 | 31 Dec | $1.0487 | ||

| 2003 | 08 Jan | $1.0377 | 31 Dec | $1.2630 | ||

| 2004 | 14 May | $1.1802 | 28 Dec | $1.3633 | ||

| 2005 | 15 Nov | $1.1667 | 03 Jan | $1.3507 | ||

| 2006 | 02 Jan | $1.1826 | 05 Dec | $1.3331 | ||

| 2007 | 12 Jan | $1.2893 | 27 Nov | $1.4874 | ||

| 2008 | 10 Jan | $1.4662 | 14 Jan | $1.4895 | ||

| Source: Euro exchange rates in USD, ECB | ||||||

The ECB targets interest rates rather than exchange rates and in general does not intervene on the foreign exchange rate markets, because of the implications of the Mundell-Fleming Model which suggest that a central bank cannot maintain interest rate and exchange rate targets simultaneously because increasing the money supply results in a depreciation of the currency. In the years following the Single European Act, the EU has liberalised its capital markets, and as the ECB has chosen monetary autonomy, the exchange rate regime of the euro is flexible, or floating. This explains why the exchange rate of the euro vis-à-vis other currencies is characterised by strong fluctuations. Most notable are the fluctuations of the euro versus the U.S. dollar, another free-floating currency. However this focus on the dollar-euro parity is partly subjective. It is taken as a reference because the euro competes with the dollars role as reserve currency. The effect of this selective reference is misleading, as it gives observers the impression that a rise in the value of the euro versus the dollar is the effect of increased global strength of the euro, while it may be the effect of an intrinsic weakening of the dollar itself.

Against other major currencies

Green: in Jan-1999: €1 = $1.18 ; in Nov-2007: €1 = $1.47

Red: in Jan-1999: €1 = ¥133 ; in Nov-2007: €1 = ¥166

Blue: in Jan-1999: €1 = £0.71 ; in Nov-2007: €1 = £0.70

After the introduction of the euro, its exchange rate against other currencies fell heavily, especially against the U.S. dollar. At its introduction in 1999, the euro was traded at US$1.18/€, but by October 26, 2000, it had fallen to an all-time low of $0.8228/€. After the appearance of the coins and notes in 2002 and the replacement of all national currencies, the euro then began steadily appreciating, and reached parity with the U.S. dollar on July 15, 2002. Since December 2002, the euro has not fallen below parity with the U.S. dollar.

On 23 May 2003, the euro surpassed its initial ($1.18) trading value for the first time. At the end of 2004, it reached a 2004 peak of $1.3668 (€0.7316/$) as the U.S. dollar fell against all major currencies, fuelled by the so-called double deficit in the US accounts. But the dollar recovered in 2005, rising to $1.18 (€0.85/$) in July 2005, and was stable throughout the second half of 2005. The steep increase in U.S. interest rates during 2005 had much to do with this trend. By early December 2006, the dollar had fallen below €0.75, hitting a low of €0.7495/$ ($1.3340/€), slightly more than 3c above its record low, set in late 2004. On January 14, 2008, the dollar and British pound fell to all-time lows at $1.4895 and £0.7600, respectively against the euro (€0.6723/$).

- Current and historical exchange rates against 29 other currencies (European Central Bank)

- Current dollar/euro exchange rates (BBC)

- Historical exchange rate from 1971 until now

Currencies pegged to the euro

There are a number of non-EU currencies that were pegged to a European currency and are now currencies related to the euro: the Cape Verdean escudo, the Bosnia and Herzegovina convertible mark, the CFP franc, the CFA franc and the Comorian franc.

In total, the euro is the official currency in 15 states inside the European Union, and 5 states/territories outside the European Union. In addition, 23 states and territories have currencies that are directly pegged to the euro including 14 countries in mainland Africa, 3 EU members that will ultimately join the euro, 3 French Pacific territories, 2 African island countries and another Balkan country, Bosnia and Herzegovina.

| Use Yahoo! Finance: | AUD CAD CHF GBP HKD JPY USD SEK RUB |

| Use XE.com: | AUD CAD CHF GBP HKD JPY USD SEK RUB |

| Use OANDA.com: | AUD CAD CHF GBP HKD JPY USD SEK RUB |

In the United Kingdom, although not a member of the Eurozone, many high-street banks report that as much as 90% of their international trade is conducted in euro. It is common therefore for them to use the euro as their 'core' currency on international business systems, only converting to Sterling for local accountancy purposes.

Name and linguistic issues

The formal titles of the currency are "euro" for the major unit and "cent" for the minor (one hundreth) unit and in most Eurozone official languages, these names are invariant in the plural. These styles are often in conflict with the structures of the national languages. However, it is the policy of the EU that these national norms should continue in local documents intended for the general public. For the different national styles and related controversies, see Linguistic issues concerning the euro.